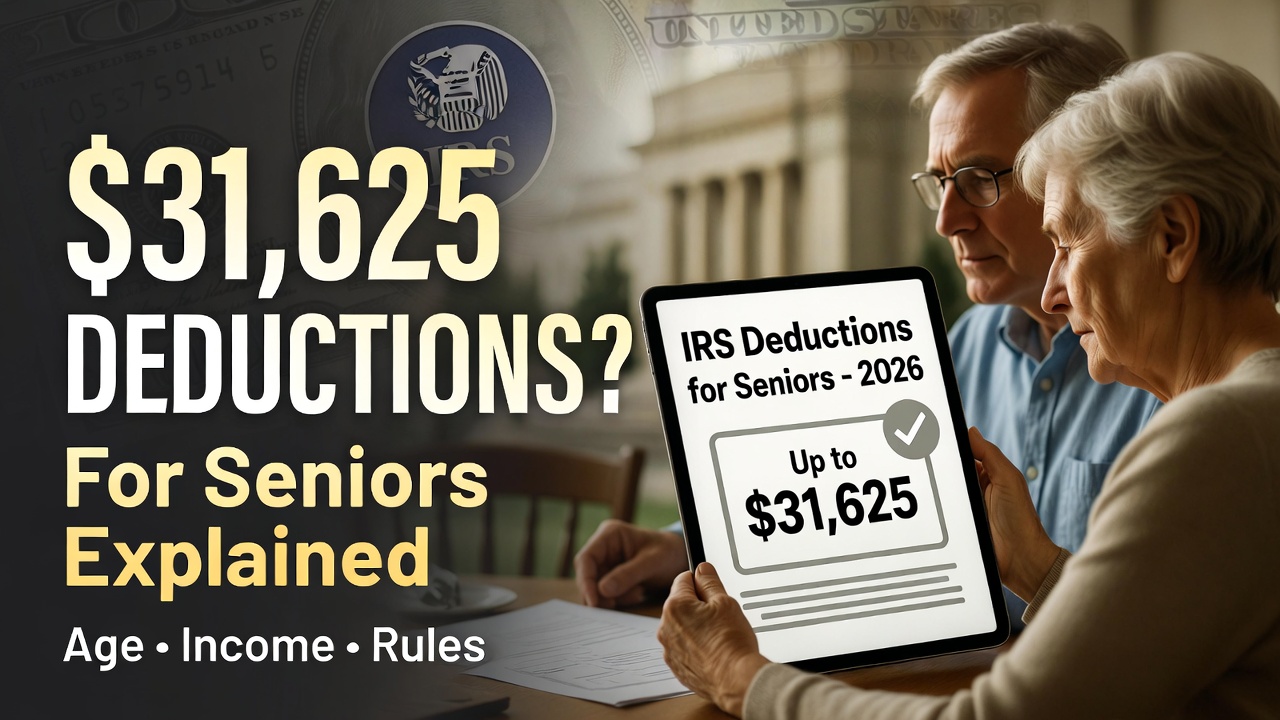

$31,625 IRS Deductions for Seniors Explained: You may have seen headlines or social media posts claiming that seniors can receive a “$31,625 IRS deduction.” This number can sound confusing and even misleading at first glance. It is not a new or automatic deduction that seniors receive just for reaching a certain age. Instead, it represents a total that can occur when several existing tax deductions are combined under very specific circumstances.

This amount is only possible for certain older taxpayers who meet age, income, and filing status requirements in a particular tax year. Understanding how this figure is created helps prevent unrealistic expectations and allows seniors to plan their taxes more accurately.

Why the $31,625 Figure Exists

The $31,625 figure most often applies to a taxpayer who is age 65 or older and files as Head of Household on a 2025 tax return, which is typically filed during the 2026 tax season. In that situation, several deductions can stack together to reduce taxable income.

This total is not guaranteed. It depends on eligibility for each deduction and whether the taxpayer has enough taxable income to benefit from them. Deductions lower taxable income, but they do not create income or refunds by themselves.

The Role of the Standard Deduction

The standard deduction is the foundation of the $31,625 total. It is a fixed amount that reduces taxable income for taxpayers who do not itemize deductions. For the 2025 tax year, the standard deduction for a Head of Household filer is $23,625.

This base deduction applies regardless of age. Many seniors use the standard deduction because it is often higher and simpler than itemizing expenses. Without this base amount, the larger total would not be possible.

The Extra Standard Deduction for Being Age 65 or Older

Taxpayers who are age 65 or older by the end of the tax year qualify for an additional standard deduction. This extra amount recognizes that older adults often have different financial needs and expenses.

For the 2025 tax year, the extra deduction is $2,000 for individuals who are unmarried and not a surviving spouse. This amount is added on top of the base standard deduction, further reducing taxable income. The IRS considers a person to be 65 the day before their 65th birthday, which can matter for year-end birthdays.

The Temporary Enhanced Deduction for Seniors

Beginning in 2025, a temporary enhanced deduction for seniors was introduced. This deduction allows eligible individuals age 65 or older to claim up to an additional $6,000. Married couples filing jointly may claim up to $12,000 if both spouses qualify.

This enhanced deduction is separate from the standard deduction and the extra age-based amount. It can be claimed whether a taxpayer uses the standard deduction or itemizes deductions, making it especially valuable for qualifying seniors.

How These Deductions Combine

When all three deductions apply to the same taxpayer, the total can be significant. For a Head of Household filer age 65 or older in 2025, the base standard deduction of $23,625 combines with the $2,000 age-based extra deduction and the $6,000 enhanced senior deduction.

When added together, these amounts equal $31,625. This is where the headline number comes from. However, this total only applies when all eligibility requirements are met and income levels are within allowed limits.

Income Limits and the Phaseout Rule

The enhanced senior deduction is not available at all income levels. It is subject to a phaseout based on modified adjusted gross income, often referred to as MAGI. For most individual filers, the phaseout begins once MAGI exceeds $75,000. For married couples filing jointly, it begins at $150,000.

As income rises above these thresholds, the enhanced deduction is reduced. The reduction is calculated at a rate of six percent of the amount by which income exceeds the threshold. Once income exceeds the threshold by $100,000, the enhanced deduction is fully phased out and reduced to zero.

Why Filing Status Matters

Filing status plays a major role in determining deduction amounts. Head of Household status provides a higher standard deduction than single filing status, which is why the $31,625 example often applies to that group. Married couples must file jointly to claim the enhanced senior deduction.

Married taxpayers who file separately are not eligible for the enhanced deduction. This rule catches many people off guard and can significantly change the outcome of a tax return if the wrong filing status is used.

Common Misunderstandings About the $31,625 Amount

One of the biggest misconceptions is that every senior automatically qualifies for a $31,625 deduction. This is not true. The amount depends on age, filing status, income level, and eligibility for the enhanced deduction.

Another common misunderstanding is confusing the extra age-based standard deduction with the enhanced senior deduction. These are two separate benefits, and while they can stack together, they follow different rules and calculations.

How the Deduction Appears on a Tax Return

For the 2025 tax year, the enhanced senior deduction is calculated using a specific worksheet and reported on a dedicated schedule that flows into the main tax form. Most taxpayers do not need to file special requests or explanations.

As long as age, income, filing status, and Social Security number information are correct, the calculation is handled as part of the standard tax preparation process. Errors usually occur when income is misreported or filing status is chosen incorrectly.

Why Understanding This Matters

Knowing how the $31,625 total is created helps seniors set realistic expectations. It also helps avoid disappointment caused by misleading headlines that imply guaranteed benefits. For those who do qualify, the combined deductions can significantly reduce taxable income and overall tax liability.

For others, understanding the income phaseout explains why the amount may be smaller or unavailable. This clarity allows for better financial planning and informed tax decisions.

The “$31,625 IRS deduction for seniors” is not a single special program or automatic benefit. It is a possible total that results from stacking the standard deduction, the extra age-based standard deduction, and the temporary enhanced senior deduction in a specific tax year. Eligibility depends on age, filing status, income limits, and proper filing.

Once these rules are clearly understood, the number becomes far less mysterious. Seniors who meet the requirements may benefit significantly, while others can better understand why they do not qualify for the full amount.

Disclaimer

This article is for informational purposes only and does not provide tax, legal, or financial advice. Tax laws, deduction amounts, and eligibility rules may change and can vary based on individual circumstances. Readers should consult the official IRS website or a qualified tax professional for personalized guidance.