2026 Social Security COLA: Inflation in the United States has slowed compared to previous years, but many Americans may still struggle financially in 2026. Prices for everyday needs such as housing, food, and healthcare remain high, especially for retirees living on fixed incomes. Although Social Security benefits are expected to increase next year, rising Medicare costs could reduce the real value of that increase.

For millions of beneficiaries, the expected cost of living adjustment may not bring the relief they are hoping for. Understanding how Social Security and Medicare interact is important for realistic financial planning.

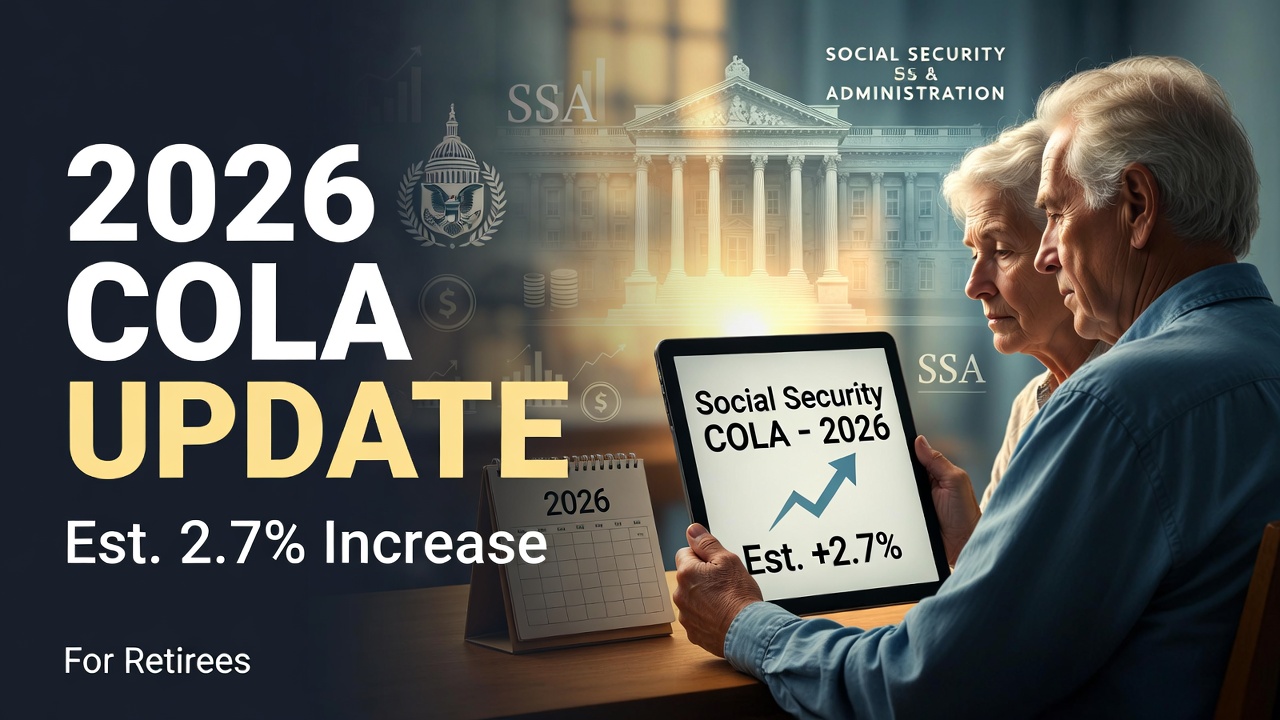

Estimated Social Security Increase for 2026

Based on recent inflation data, the Social Security cost of living adjustment for 2026 is currently estimated at 2.7 percent. This estimate has increased slightly from earlier projections, reflecting updated inflation figures. The increase is linked to the Consumer Price Index for Urban Wage Earners and Clerical Workers, which tracks changes in prices faced by working households.

While a 2.7 percent increase sounds helpful, it is considered modest compared to adjustments seen during periods of higher inflation. For many beneficiaries, this increase may not keep pace with rising living costs.

Why the COLA Estimate Is Rising

The COLA estimate increased due to recent inflation trends. In June, the CPI-W rose by 2.6 percent compared to the previous year. Overall inflation reached 2.7 percent, higher than earlier months. These changes reflect ongoing price pressures in several key areas of the economy.

Housing expenses, service costs, and medical care prices continue to rise, even as energy prices have eased. These mixed economic conditions have pushed inflation slightly higher, leading to the revised COLA estimate for 2026.

How the Federal Reserve Fits Into the Picture

The Federal Reserve continues to aim for a long-term inflation rate of around 2 percent. However, reaching that goal has been difficult due to ongoing economic challenges. Supply chain issues, labor costs, and demand for services have kept prices elevated.

As long as inflation remains above target, Social Security adjustments are likely to continue, but they may not fully reflect the actual cost increases experienced by retirees, especially in healthcare.

Medicare Part B Premiums Expected to Rise

One of the biggest concerns for Social Security recipients is the projected increase in Medicare Part B premiums. According to official estimates, premiums could rise from $185.00 in 2025 to $206.50 in 2026. This would be an increase of $21.50 per month.

This jump represents an increase of more than 11 percent, making it one of the largest Medicare premium hikes in recent years. Higher premiums often offset Social Security increases, limiting the financial benefit for retirees.

How Higher Medicare Costs Affect Benefits

Medicare Part B premiums are usually deducted directly from Social Security payments. When premiums rise sharply, they can absorb most or all of the COLA increase. As a result, beneficiaries may see little change in their monthly take-home amount.

In some cases, retirees may feel like their Social Security increase has disappeared entirely. This creates frustration, especially when other living expenses continue to climb.

Understanding the Hold-Harmless Rule

The federal hold-harmless rule is designed to protect Social Security recipients from seeing their benefit payments decrease due to higher Medicare premiums. This rule ensures that a person’s net Social Security payment does not go down from one year to the next because of premium increases.

However, the rule does not guarantee a meaningful increase. It only prevents a reduction. For many beneficiaries, especially those with smaller payments, the COLA may be fully absorbed by Medicare costs.

Impact on Low-Income Beneficiaries

Low-income Social Security recipients are likely to be affected the most in 2026. Individuals receiving less than $800 per month may find that their entire COLA increase goes toward higher Medicare premiums. This leaves little or no extra income to cover rising prices in other areas.

Although the average Social Security benefit is higher, many recipients receive less than the average. For these individuals, even small increases in healthcare costs can have a serious financial impact.

How the Social Security COLA Is Calculated

The Social Security Administration calculates the annual COLA using inflation data from July, August, and September. These months are compared to the same period from the previous year. The average increase determines the final adjustment.

The official COLA announcement is typically made in October. While the current estimate is 2.7 percent, the final number could change depending on inflation data released later in the year.

Why Small Percentage Changes Matter

More than 74 million Americans rely on Social Security benefits. Because of this large population, even small changes in the COLA have wide-reaching effects. A difference of a few tenths of a percent can impact billions of dollars in total benefits.

For individual households, these changes influence budgeting decisions, savings plans, and healthcare choices. Understanding the numbers helps beneficiaries prepare for what lies ahead.

Preparing for 2026 Benefit Changes

Retirees can take steps to prepare for potential changes in 2026. Staying informed about inflation trends and Medicare announcements can help manage expectations. Reviewing healthcare coverage and understanding how deductions affect net benefits is also important.

Planning ahead may help reduce financial stress, especially for those living on limited incomes. Awareness and preparation can make a significant difference.

Looking Ahead to the 2026 Outlook

While a 2.7 percent COLA provides some protection against inflation, it may not deliver meaningful relief for many Americans. Rising Medicare premiums threaten to reduce or eliminate the increase for millions of beneficiaries.

As healthcare costs continue to rise, Social Security recipients may need to rely on careful budgeting and informed planning to maintain financial stability in 2026.

The expected 2026 Social Security cost of living adjustment offers modest inflation relief, but higher Medicare premiums could significantly reduce its impact. Low-income beneficiaries are especially vulnerable, as healthcare costs may absorb most of their increase. Staying informed about inflation data, Medicare changes, and benefit rules is essential for navigating the year ahead with confidence.

Disclaimer

This article is for informational purposes only and does not provide financial, legal, or retirement advice. Social Security benefits, Medicare premiums, and inflation estimates are subject to change based on official government decisions and economic conditions. Readers should consult official Social Security Administration and Medicare resources or speak with a qualified professional for personalized guidance.